ING Bank Manila is seeing higher growth for the Philippines this year but banking giant HSBC thinks otherwise, forecasting a contraction.

ING Bank Manila is seeing higher growth for the Philippines this year but banking giant HSBC thinks otherwise, forecasting a contraction.

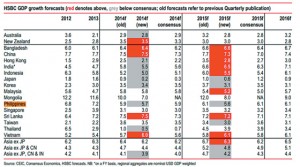

ING said GDP growth this year will improve to 6.7 percent from its own estimate of 5.8 percent growth last year.